Buying a House, Part 2

In Part 1, I briefly talked about the need to interview the people you are going to be working with. In one of the In a case of “not prioritizing like most people”, I was actually quite looking forward to looking for a good insurance provider. As renters, we have tenant insurance which is intended to protect your belongings but really, with all of the limitations, it might as well be throwing money away. Aside from the coverage itself, the fact that it was exceedingly difficult to extract explicit coverage information was the driving force to look elsewhere.

Quick Links

Where we started: AllState

Just like with home buying, it’s super important to identify the things you care about and really dig into the specifics of the type of coverage you are getting. This is doubly so if, like many people, you’re going to select a provider and not shop around regularly for better options. In our case, tenant insurance was an extremely cut down version of homeowners insurance so I was pretty eager to explore what kind of peace of mind we could get with the ‘full fat’ homeowner insurance. Obviously, with homeowner insurance, there is going to be a broader coverage base (i.e., the home!) but at this time, I was exploring coverage for “stuff”.

With tenant insurance, they ask you a fairly standard barrage of questions to get a picture of the house

Address, type of house, how many rooms

Distance from hydrant, smoke detectors, any smokers

Type of heating

Whether or not you’re running a business

The number of finished rooms will the primary driver for how much contents protection you get:

One provider might get allot you $7K per room, so for a 2-bedroom apartment, you get $14K worth of ‘stuff protection’

Another provider might allot you $8K for your 4-bedroom rental giving you $32K of coverage

All of the other questions contribute to calculating the premium. In some cases (many?) you might want to increase this topline number - at a cost (of course!). Regardless of what your final topline number is, there are a ton of limitations, caveats, annoyances and gotchas. You really need to drill down and understand your risk/coverage comfort level when it comes to protecting stuff. In our case, I wanted to look at four broad categories:

Tools and Yard equipment

Kitchen stuff

Camera gear (specifically) and most importantly

Computers

Annoyances to watch out for

Joint Accounts

One annoying thing I found was that with my provider, all people living the house were included on the insurance whether I wanted it or not. From a risk perspective, this makes sense i.e., is Roommate Bob is a smoker, sure that would put the whole house at a higher risk and thus, my stuff would be a higher risk and I get that. But when I’m paying for insurance, I only want my stuff to be covered - Roommate Bob can go get his own damn coverage.

When I first went into setup insurance, there was just my car insurance and the joint tenant insurance and I paid for it on the spot; later on, we added the second car insurance account. You would think that, when getting the accounts setup in their computer system, they would do some of the following:

Two accounts: one for my car and our joint tenant and a second for her car insurance

Three accounts: one for each coverage

Nope. The system took the nonsensical route of ‘associating’ the tenant insurance with her auto insurance and there was no way to change it. Is this a big deal? Nope. But if your system is so crippled that you can’t get the little things right, maybe it can’t get the big things right either.

For us this isn’t ultimately a big deal but this could totally be disastrous in other scenarios where there is a breakdown of the relationship and one partner simply doesn’t renew/pay for the tenant insurance and the other partner is none the wiser.

Are you running a business?

So much of insurance hinges on whether or not you’re running a business. It’s ‘obvious’ if you have customers entering for goods and/or services; those are easy scenarios. The modern ‘gig’ and ‘creator’ economy makes things tricky. Consider whether the following scenarios would count as operating a business at home:

I’m a full-time Youtuber who streams gaming from home. My computer and streaming equipment could be business assets. Of the examples, this might be the most clear cut case.

I’m a full-time vlogger who uploads using an iPhone. Is the iPhone considered a business asset? What if I vlog from my living room, does that mean I’m operating a business from home? What if I walk out to the sidewalk - that wouldn’t be at home anymore right?

I have a full-time job that pays the bills, but I found a neat Instagram niche and get a monthly kickback. Is that a business at home? What if it was a $100K/month kickback? What if I walk out to the sidewalk, is my iPhone considered a piece of business equipment?

What if I take pictures en-masse and upload them to stock-photo websites and don’t think about it? What if nobody buys my photos? What if one of my photos hits jackpot in a years time?

What if my kid mows the lawns in the neighborhood for $20? Does it change anything if the kid gets $10K/lawn?

This is a QA brain at work when the definition of “operate a business at home” or “equipment for business purposes” hasn’t been updated by the insurance industry at large in a decade. The frustrating answer is often that it depends but we won’t tell you what it depends on.

Limits

The limits for my AllState tenant insurance range from pretty paltry to being totally out there. I pulled out a few from the ‘Special Limits of Insurance’ section. AllState says that the coverage limits for tenant insurance ‘provide sufficient coverage for the average person’.

There are some easy ones which makes sense:

Jewelry - $7K cumulative, max $2.5K per item. Jewelry is the category that I find everyone focuses on. While I think the numbers here are on the low side, this limitation has been in play for so long now that it’s now 'just the way it is’

Cash, money, bouillon - $1K cumulative. Keep this in mind if you keep emergency funds at home.

There are some categories that are over-covered

Computer software - $5K cumulative. This refers to the cost of replacing software (i.e., Adobe Photoshop license) due to computer loss and doesn’t cover data recovery. LOL if my parents delete my Steam account, can I use this as recourse? Seriously though, if you have $5K of computer software, then you should have some form of backup to handle this. It’s not hard, and certainly not expensive to do this.

There are some categories that I think could have been better distributed i.e., lower the standard coverage amount of but add an endorsement package that increases the coverage for people who need it to a level that is more appropriate

Tractors/Snowblowers - $10K cumulative. This either seems too low or too high and if I were in charge, I would have dropped this down to $6K but also made a “landscaping package” to bring it up to $25K.

Bicycles - $2K per. I suspect that $2K per bike is excessive for your run of the mill bike but at the same time, once you get into serious road-bikes, $2K is pretty underwhelming, so maybe have a “cyclist endorsement” to bring it up to $10K per bike

And finally some categories that can get you into coverage trouble if you’re not paying attention

Spare auto parts - $1K cumulative. On first blush I thought “that’s okay, I don’t keep spare mufflers or clutch packs in my garage” but then you realize snow tires count as spare auto parts…

Photography equipment - $1K cumulative. For ‘real’ cameras, this is comically low. Even if you look at the camera that most people have — their smartphone — it’s quite inadequate coverage.

Amusing thought: a smartphone would likely not be considered ‘photography equipment’ even though it takes pictures (perhaps the argument is that it does ‘other’ things?) Makes me wonder if you had something like a Canon C300 video camera or a DJi Inspire 2 drone or an go up in smoke, it would get classified as a photography equipment.

Personal Article Floaters (PAFs)

So to work around the comically low coverage for certain items (i.e., camera gear) or for categories you have specific concerns about (i..e, computer equipment), providers give you the option of adding a personal artifacts floater or PAF at additional cost (of course!). The headache doesn’t end here though as there are sometimes more hoops to jump through (depending on your provider):

Items over a certain amount needed to have an appraisal (and there’s no guidance on how to go about this). In the case of my recently purchased camera at the time, I simply went back to the store I bought it from and nicely asked for a “buyback quote”

Having a PAF would reduce the deductible for that specific item to $0 in case of a loss however, the premium was ~1% of the amount per-year. For a singular high-value item, this might be something to consider but multiple cameras and lenses, this becomes infeasible very quickly

Computers, specifically

Tying all of this together is how they treat computers. From an accounting perspective, computers depreciate something like 25% a year. If we do simple math, this would put it approximately 0-value after four years. For the large majority of computers out there — off the shelf desktops and more so, laptops, this is totally true.

However, once you start getting into the custom built space where specific parts are chosen to hit specific price/performance targets, all bets are off. It’s absolutely laughable that a $10K computer purpose-built as a high-performance machine, would be outclassed by an el-cheapo in four years.

Funny anecdote: modern computers are funny creatures. They ‘get more work done’ (and do so for less power consumption) but there is such an emphasis on ridiculously lower and lower power envelopes that in the field, they don’t get more work done. I had a Q6600 (circa-2008) based machine outperforming my work laptop from 2018 with an “i7”. Apples to apples? No. But winning is winning.

I don’t expect computers, even high-performance custom built ones to last forever. Instead, I was looking for a confirmation that the process would bring in someone who knew something about computer hardware.

Monitored Security

This one is amusing and feels like it’s just one industry feeding another: security systems. There’s a discount of some sort provided if you have a professionally monitored security system for your home. This by itself is fair and makes sense but the insurance industry as a whole makes it very clear that you do not qualify for any discount if you any self-monitored (i.e., smartphone) security system.

Again, this by itself is a tiny bit annoying and starts to feel like it’s a bit of a ‘you scratch my back’ industry behavior, I can understand that. Most people would not have the same perceived (that’s the critical word there) level of service that a monitored security system might have so it’s justifiable. What if we went on the other end of the security spectrum? I checked!

Multi-point locks on your doors? No discount

Breach resistant doors? No discount

Ballistic/shatter resistant glass? No discount

Mantrap entrance? No discount

Panic room? No discount

Bollards? No discount

Actual security guards with a canine unit patrolling the grounds 24x7? No discount

A platoon of actual soldiers stationed in your garage, complete with air support? No discount.

But hey, if you sign up for ADT, you qualify for a discount.

On a similar note, a few years ago when I was doing some preliminary checks on life insurance, I asked about these things as well as wearing ballistic rated clothing, having bodyguards, on-call doctors and up-armoring personal vehicles — no discount (even if you live in stereotypical Detroit — I specifically asked). But hey, if your cholesterol is high, your rate is going up.

I don’t really blame the agents, they just pitch the policy they have to work with, the problem comes down from on top. Risk analysis is a fickle subject that focuses on penalizing the higher risk scenarios (rightly so) but doesn’t do enough to incentivize the other end of the spectrum.

Getting specific details is like pulling teeth

This is the big one: trying to understand what is covered and how it’s covered can be like pulling teeth.

Obviously your experience will vary wildly from provider to provider or even from agent to agent but when it’s bad, it’s bad. In some cases, there’s very much a “don’t worry, this is complicated but the point is, you’re covered” — until you’re not.

I understand and can appreciate that the process is complicated, but the lack of transparency is brutal. Here are my favorites:

“Any product that involves generation of income will be reviewed and determined by Claims Advisor at the time of loss. Therefore could be considered as business tool and may not qualify as personal contents”

“PAF is not available for personal computer”

LOL if you get a text from your boss asking if you want some extra shifts, that phone is now involved in the generation of income. Will it likely rule that way? Probably (hopefully!) not, but the industry reserves the right to judge however it sees fit.

Again, the experience here will vary wildly depending on the agent you’re working with - some are awesome and will go the extra mile to get you a full picture and even if the premium ends up being a bit more, sometimes that extra effort is worth it.

Comparing Quotes - Use a Standardized Template

Just like how finding a good realtor you can work with, you have confidence in and is a good fit in general is crucial to the peace of mind during the house buying process, I think finding a good insurance agent or broker is super crucial in the insurance process. In the process of finding insurance, I would be working with two different types of people:

Agent - represents a single insurance provider

Broker - doesn’t represent an individual provider, but rather, combs the insurance market as a whole, to (theoretically) find you the best coverage across multiple providers

For all intents and purposes, as a consumer, the terms are effectively interchangeable — at the end of the day, it’s a person I talk to in order to get an insurance quote from. As a non-expert, I thought that working with a broker is the way to go since you have access to ‘the whole market’.

I can’t recommend this enough: shop around! Anything less than three quotes and you’re selling yourself short. One thing I didn’t expect was how wildly different the coverage was between different providers for the aspects I cared about. As such, it’s super important that you [a] figure out what things you want coverage for (and what kind of coverage you would want) and then [b] find out, very specifically, what your coverage is.

I found it most effective to come up with a standard set of data to provide with every candidate. Use this opportunity to preemptively field any questions and concerns — how a potential agent or provider tackles the questions and concerns has an intangible value. Here’s what the information I provided and how I broke it down for each agent.

Information

Address

Age of Home/When was it built

Square footage

Closing date

Construction

Brick, vinyl siding, etc.

Finished basement? Does the above square-footage include the basement?

How many full baths? Half baths?

Sump pump? Battery backup? Backflow preventer? Leak-detection system?

Is there a front porch? Size?

Is there a rear deck? Size?

Pool? Hottub? Are either of these built-in?

Furnace type (gas/electric) and age

Age of the air-conditioner

What type of roof (asphalt/steel/fiberglass etc) and age

What type of electrical service is there (100A? 200A?)

Copper vs Aluminum wiring? Breaker vs fuse box?

Is there in-floor heating?

What type of water heater is it (gas/electric)? How old is it?

Auxiliary heaters (i.e., propane heater in the garage)

What type of plumbing (copper? pex?)

What size garage? Attached/detached?

Other

Do you plan on moving in right away? Or will there be pre-renovations?

Smokers in the house? Any grow-ops?

Who’s gonna live there (primary vs tenants)

Will there be a business on premise?

Will there be a mortgage on the house? Birthdates for mortgagees

Distance to closest fire hydrant? Some want to know distance from fire-hall

Fire extinguishers?

Is anyone working from home? (i.e., due to covid)

If you’d like to consider bundling auto coverage

VIN and driver’s license for the primary driver for each vehicle you might want to add

Whether or not you would do any kind of drive-monitoring

What kind of yearly mileage you typically expect

Whether or not you have any 3rd party alarm or tracking systems installed on any of the vehicles

Quotes Requested

House only

House + cars (if applicable)

Willing/preference to pay upfront for insurance vs monthly

Make sure to compare the same liability-coverage across all of the candidates

The makeup of a quote

So at this point in the insurance process, all of the bits of information are entered into a system which then spits out a a quote. For me the big ticket items are:

The house

Related structures (i.e., shed)

Contents (my ‘stuff’)

Additional living expenses (coverage that kicks in when you can’t stay at your home due to things like an evacuation order)

Sometimes quotes will use slightly different terminology but the gist will be the same. Of these, the most important number is the ‘house’ number — all of the other coverages are calculated as a percentage of that (with each provider having their own distribution). Specifically with respect to covering ‘stuff’, you can add floaters and endorsements etc. that will provide you with additional specific coverage but all of that comes at yet an additional cost. There are ‘settings’ you can ask for that will directly scale the baseline house amount but for a first pass, I let the agents do what they see fit — it’s their bid so to speak.

Exploring the limitations of contents coverage

Now that you have a handful of quotes and after you (optionally) rule out the quotes that were ‘needlessly difficult’ to get, you can narrow down the quotes by digging into the contents categories that matter to you. Obviously everyone will be different, for me, my categories were cooking, woodworking, photography and computers.

Note that poking and prodding into the details for the coverage of these categories will shed some light on the fit of the agent, and by proxy the provider. Sometimes, it’s less frustrating to take your business elsewhere purely based on the experience from a single agent. I recommend using large numbers to make a point but stay within the realm of possibility. In my example, I have a hypothetical cumulative of 210K worth of contents I wanted to explore:

$10K in cooking equipment (knives, pots, pans, appliances)

$50K in camera and photo equipment

$50K in power and yard tools

$100K in computers

For computers, it’s important to note that this is hardware only, not data. Lots of providers will get stuck up on “we don’t offer data insurance” - lol, data can be ballparked at $1M/GB anyways so that’s going to ruin your day ;) To keep thing simple, I wanted to keep this scoped to something a real, physical, thing.

If it’s true, make sure to flag that these are not for business.

At the end of the day, you’re looking to understand whether or not ‘your stuff’ (with an example value of 210K) will fit in the quoted contents coverage amount and if there are any limitations. The coverage can vary wildly between particular providers. For example, with computers I had two extremes:

Some quotes come back with “we don’t care: if the computer fits inside the contents amount, it’s covered” (assuming proper documentation etc.)

On the other extreme, I had another provider come back with “cumulative $5K for computers”. — RIP any households with one or more macbooks right?

The experience of digging for additional details may also lead you to eliminate potential providers — and it should (if the experience was like pulling teeth).

Data!

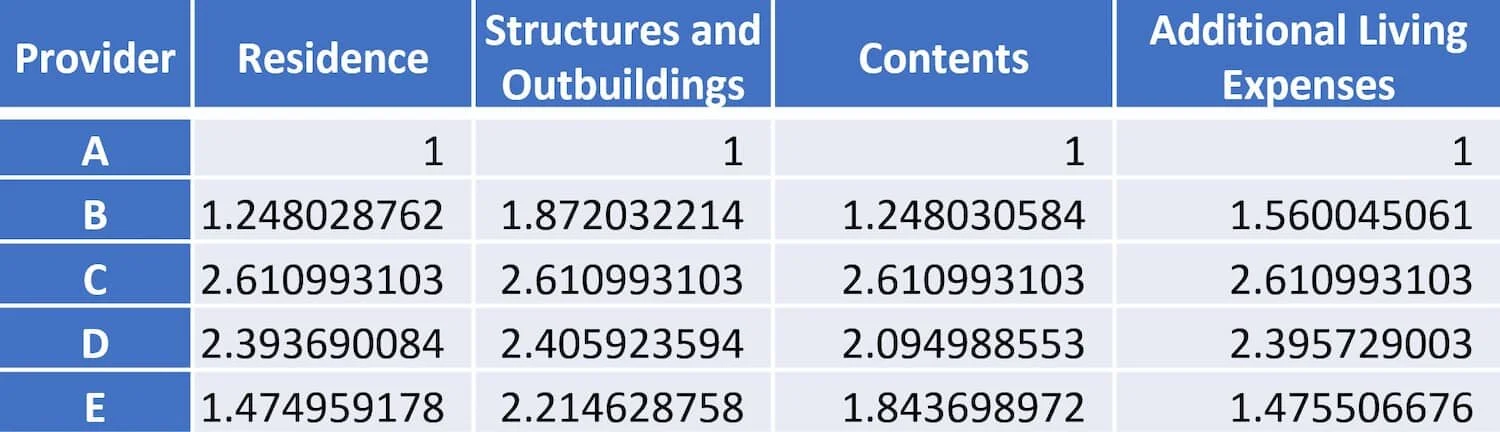

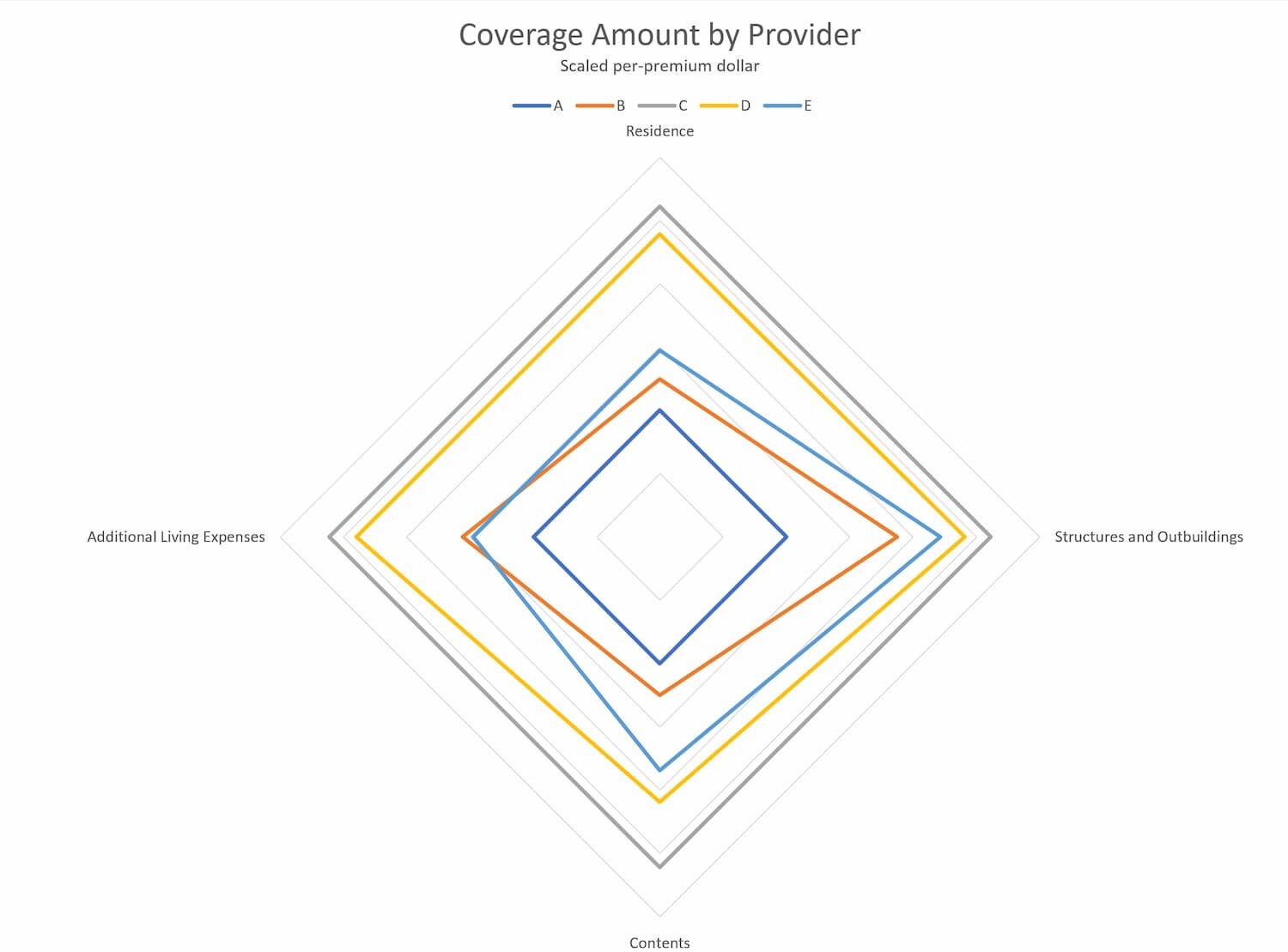

Once you’ve narrowed down the candidates - we can plot out all the major coverage blocks. By expressing the amounts relatively, it’s very easy to see where the value shift is (and makes it easier to compare on a blog by removing geographic price scaling from the picture):

If we remember from before, the ‘Residence’ value is what drives the remaining limits and each provider arrived at wildly different values. One way we can look at this is to rescale the coverage to account for the different residence values. In essence, this is comparing the distribution for each provider independent of the premium.

Here we can see that, if all of the providers valued the house at the same amount, ‘Provider E’ would have a landslide advantage for contents protection and if we were to prioritize additional living expenses, ‘Provider B’ would be the frontrunner:

However, the reality is that the providers didn’t value the residence at the same amount and while we could get them to increase the valuation that would come at an additional cost and it wouldn’t be a fair-comparison (since we could just ask the better proposition option to do the same).

Spoiler: Provider E ended up having the absolute worst computer-specific limits: $5K cumulative.

Instead of ‘coverage distribution’, we need to find a better metric. Providers set the premium so if we scale for that, we can get a picture for “how much coverage do we get per premium-dollar”. Here, we can see a runaway win for Provider C and to a lesser degree, Provider D.

While there is a lot more to deciding on a provider (sometimes, you’re getting what you’re paying for!) this can certainly give us an indication of which providers to initially start our search with. By having a large sample of quotes to work with, you can get a consider a larger pool of options.

What about the rest of the coverage?

Coming from tenant/renters insurance, I’m most familiar with the aggravation of getting coverage for ‘stuff’ but there’s certainly much more to consider: water (above and below), ice etc. Every region will and household will be unique so it’s super critical to go through the policy with almost a combative lens and making sure you understand and are comfortable with the various potential gotchas. Ask tons of questions! In my specific case, I got lucky as most of the coverage policies were roughly all in line with each other (or the short-list had the better options).

Trim Level

One thing to consider is the general ‘nice-ness’ of your home, measured in vague terms like “average”, “above average” etc. Depending on how the home’s interior is described, this will directly impact the baseline ‘residence’ number which in turn, will boost coverage to contents, freestanding structures etc.

The ‘trim level’ of your home goes hand in hand with a ‘Guaranteed Replacement Cost’ attribute on your policy: if you don’t accurately describe your home’s trim level, then you run the risk of having the building replacement not being to the same level. Will it be a house? Yes. Will it have quartz countertops? Likely not. You’ll have to decide on your own risk tolerance.

Inventory Management

Going hand in hand with contents protection, it’s super important to have some form of inventory management for your belongings. Having a way to document and prove your belongings is critical in a loss-situation. I explore this in my previous post, Keeping Inventory.

Reducing your premiums

This is ultimately what it’s about: we’ve looked at getting the best coverage for your situation but at the end of the day, there will always be the premium.

Ask tons of questions — you’re about to spend a ton of money on the promise that some organization will have your back when you need them. When things go south is not the time to be finding out your coverage preconditions and limitations for the first time.

Search around, get a whole whatload of quotes: get some recommendations, do some manual research of specific providers, look up some insurance brokers and to round this all off, visit a robo-quote system like Ratehub. You don’t need to follow through with the computer generated quotes but that can certainly introduce you to a bunch of providers that you might not have naturally discovered

Ask your agent/broker directly for different ways you can save on your premium. Ask people who have the same provider how they’ve saved on their premiums too. This can be a really telling moment with the broker/agent you’re working with — with AllState, I asked open ended questions about reducing the premium and beyond “pair home and auto together”, my agent couldn’t think of anything until I gently ‘reminded’ him about all the different ways (some of which he had brochures all around his desk)

Recommendations

I’ve mentioned a few times that a good agent/broker experience brings a certain value into the equation (and conversely, a bad experience can skew the value proposition substantially i.e., if you’re a jerk, you’re not going to get my business). I’ve said that one of the most important things you can do is ask tons of questions - it your only real opportunity to find out details on your coverage on your terms - before you pay into it.

My interactions with Tim have been nothing short of exemplary - and I did not go easy on him. He addressed my concerns both literally (digging further for answers as needed) but also leveled with me as a person, addressing the underlying concern.

Tim Howard, Insurance Advisor w/ Heartland Farm

Working with Tim has been great: he answered all of my questions and went a step further to address the underlying concerns. Tim went above and beyond to make sure his answers were well-rounded and specific to my questions without resorting to text-book/easy/cookie-cutter scenarios.

Working with Tim, it was easy to have confidence that the coverage I ended up with was tailored to my needs.